| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

Delaware

|

26-0734029

|

|

(State or Other Jurisdiction of

|

(I.R.S. Employer

|

|

Incorporation or Organization)

|

Identification No.)

|

|

850 Shades Creek Parkway, Birmingham, Alabama

|

35209

|

|

(Address of Principal Executive Offices)

|

(Zip Code)

|

|

Large accelerated filer ¨ Accelerated filer x Non-accelerated filer ¨ Smaller reporting company ¨

|

|

Class

|

|

Outstanding as of February 28, 2014

|

|

Common stock, $.001 par value

|

|

7,420,812

|

|

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

|

3

|

|

|

|

|

|

|

PART I.

|

|

4

|

|

|

|

|

|

ITEM 1.

|

BUSINESS

|

4

|

|

ITEM 1A.

|

RISK FACTORS

|

25

|

|

ITEM 1B.

|

UNRESOLVED STAFF COMMENTS

|

38

|

|

ITEM 2.

|

PROPERTIES

|

38

|

|

ITEM 3.

|

LEGAL PROCEEDINGS

|

39

|

|

ITEM 4.

|

MINE SAFETY DISCLOSURES

|

40

|

|

|

|

|

|

PART II.

|

|

40

|

|

|

|

|

|

ITEM 5

|

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

|

40

|

|

ITEM 6.

|

SELECTED FINANCIAL DATA

|

42

|

|

ITEM 7.

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

44

|

|

ITEM 7A.

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

62

|

|

ITEM 8.

|

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

|

65

|

|

ITEM 9.

|

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURES

|

107

|

|

ITEM 9A.

|

CONTROLS AND PROCEDURES

|

107

|

|

ITEM 9B.

|

OTHER INFORMATION

|

108

|

|

|

|

|

|

PART III.

|

|

108

|

|

|

|

|

|

ITEM 10.

|

DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

108

|

|

ITEM 11.

|

EXECUTIVE COMPENSATION

|

108

|

|

ITEM 12.

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS

|

108

|

|

ITEM 13.

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE

|

108

|

|

ITEM 14.

|

PRINCIPAL ACCOUNTANT FEES AND SERVICES

|

108

|

|

|

|

|

|

PART IV.

|

|

109

|

|

|

|

|

|

ITEM 15.

|

EXHIBITS AND FINANCIAL STATEMENT SCHEDULES

|

109

|

|

|

|

|

|

SIGNATURES

|

111

|

|

|

|

|

|

|

EXHIBIT INDEX

|

112

|

|

| 2 | ||

| · | the effects of the continued slow economic recovery and high unemployment; |

| · | the effects of continued deleveraging of United States citizens and businesses; |

| · | the effects of potential federal spending cuts due to the United States financial budgetary “sequester”; |

| · | the effects of continued depression of residential housing values and the slow market for sales and resales; |

| · | credit risks, including credit risks resulting from the devaluation of collateralized debt obligations (CDOs) and/or structured investment vehicles to which we currently have no direct exposure; |

| · | the effects of governmental monetary and fiscal policies and legislative and regulatory changes; |

| · | the effects of hazardous weather such as the tornados that struck the state of Alabama in April 2011 and January 2012; |

| · | the effects of competition from other commercial banks, thrifts, mortgage banking firms, consumer finance companies, credit unions, securities brokerage firms, insurance companies, money market and other mutual funds and other financial institutions operating in our market area and elsewhere, including institutions operating regionally, nationally and internationally, together with competitors offering banking products and services by mail, telephone and the internet; |

| · | the effect of any merger, acquisition or other transaction to which we or any of our subsidiaries may from time to time be a party, including our ability to successfully integrate any business that we acquire; |

| · | deterioration in the financial condition of borrowers resulting in significant increases in loan losses and provisions for those losses; |

| · | the effect of changes in interest rates on the level and composition of deposits, loan demand and the values of loan collateral, securities and interest sensitive assets and liabilities; |

| · | the effects of terrorism and efforts to combat it; |

| · | the results of regulatory examinations; |

| · | changes in state and federal legislation, regulations or policies applicable to banks and other financial service providers, including regulatory or legislative developments arising out of current unsettled conditions in the economy, including implementation of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”); |

| · | the effect of inaccuracies in our assumptions underlying the establishment of our loan loss reserves; and |

| · | other factors that are discussed in the section titled “Risk Factors” in Item 1A. |

| 3 | ||

| 4 | ||

| 5 | ||

| · | the availability of successful, experienced bankers with strong reputations in the market; and |

| · | the economic attributes of the market necessary to drive quality lending opportunities coupled with deposit-related attributes of the potential market. |

|

|

|

|

|

|

|

|

|

Compound

|

|

|

|

|

|

|

|

|

|

|

Annual

|

|

|

|

|

2013

|

|

2003

|

|

Growth Rate

|

|

||

|

|

|

(Dollars in Billions)

|

|

||||||

|

Jefferson/Shelby County, Alabama

|

|

$

|

24.8

|

|

$

|

16.3

|

|

4.29

|

%

|

|

Madison County, Alabama

|

|

|

6.1

|

|

|

3.7

|

|

5.13

|

%

|

|

Montgomery County, Alabama

|

|

|

6.5

|

|

|

3.6

|

|

6.09

|

%

|

|

Houston County, Alabama

|

|

|

2.2

|

|

|

1.3

|

|

5.40

|

%

|

|

Mobile County, Alabama

|

|

|

6.0

|

|

|

4.7

|

|

2.47

|

%

|

|

Escambia County, Florida

|

|

|

3.5

|

|

|

3.1

|

|

1.22

|

%

|

| 6 | ||

|

|

|

|

|

|

|

|

|

|

|

Market

|

|

||

|

|

|

Number of

|

|

Our Market

|

|

Total Market

|

|

|

|

Share

|

|

||

|

Market

|

|

Branches

|

|

Deposits

|

|

Deposits

|

|

Ranking

|

|

Percentage

|

|

||

|

|

|

(Dollars in Millions)

|

|

||||||||||

|

Alabama:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Birmingham-Hoover MSA

|

|

3

|

|

$

|

1,217.3

|

|

$

|

30,175.1

|

|

5

|

|

4.03

|

%

|

|

Huntsville MSA

|

|

2

|

|

|

540.8

|

|

|

6,805.7

|

|

5

|

|

7.95

|

%

|

|

Montgomery MSA

|

|

2

|

|

|

374.2

|

|

|

7,810.1

|

|

7

|

|

4.79

|

%

|

|

Dothan MSA

|

|

2

|

|

|

327.1

|

|

|

2,883.9

|

|

3

|

|

11.34

|

%

|

|

Mobile MSA

|

|

1

|

|

|

15.2

|

|

|

6,041.6

|

|

18

|

|

0.25

|

%

|

|

Florida:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Pensacola-Ferry Pass-Brent MSA

|

|

2

|

|

|

202.9

|

|

|

4,638.0

|

|

8

|

|

4.38

|

%

|

| 7 | ||

| 8 | ||

| 9 | ||

| · | the asset quality of individual loans; |

| · | changes in the national and local economy and business conditions/development, including underwriting standards, collections, and charge-off and recovery practices; |

| · | changes in the nature and volume of the loan portfolio; |

| · | changes in the experience, ability and depth of our lending staff and management; |

| · | changes in the trend of the volume and severity of past-due loans and classified loans, and trends in the volume of non-accrual loans, troubled debt restructurings and other modifications, as has occurred in the residential mortgage markets and particularly for residential construction and development loans; |

| · | possible deterioration in collateral segments or other portfolio concentrations; |

| · | historical loss experience (when available) used for pools of loans (i.e. collateral types, borrowers, purposes, etc.); |

| · | changes in the quality of our loan review system and the degree of oversight by our board of directors; and |

| · | the effect of external factors such as competition and the legal and regulatory requirement on the level of estimated credit losses in our current loan portfolio. |

| 10 | ||

| 11 | ||

| · | acquiring direct or indirect ownership or control of any voting shares of any bank if, after the acquisition, the bank holding company will, directly or indirectly, own or control more than 5% of the bank’s voting shares; |

| · | acquiring all or substantially all of the assets of any bank; or |

| · | merging or consolidating with any other bank holding company. |

| 12 | ||

| · | banking or managing or controlling banks; and |

| · | any activity that the Federal Reserve determines to be so closely related to banking as to be a proper incident to the business of banking. |

| · | factoring accounts receivable; |

| · | making, acquiring, brokering or servicing loans and usual related activities; |

| · | leasing personal or real property; |

| · | operating a non-bank depository institution, such as a savings association; |

| · | trust company functions; |

| · | financial and investment advisory activities; |

| · | discount securities brokerage activities; |

| · | underwriting and dealing in government obligations and money market instruments; |

| · | providing specified management consulting and counseling activities; |

| · | performing selected data processing services and support services; |

| · | acting as an agent or broker in selling credit life insurance and other types of insurance in connection with credit transactions; and |

| · | performing selected insurance underwriting activities. |

| · | lending, trust and other banking activities; |

| · | insuring, guaranteeing, or indemnifying against loss or harm, or providing and issuing annuities, and acting as principal, agent, or broker for these purposes, in any state; |

| · | providing financial, investment, or advisory services; |

| · | issuing or selling instruments representing interests in pools of assets permissible for a bank to hold directly; |

| 13 | ||

| · | underwriting, dealing in or making a market in securities; |

| · | other activities that the Federal Reserve may determine to be so closely related to banking or managing or controlling banks as to be a proper incident to managing or controlling banks; |

| · | foreign activities permitted outside of the United States if the Federal Reserve has determined them to be usual in connection with banking operations abroad; |

| · | merchant banking through securities or insurance affiliates; and |

| · | insurance company portfolio investments. |

| 14 | ||

| · | Assessment Base. An institution’s assessment base equals the institution’s average consolidated total assets during a particular assessment period, minus the institution’s average tangible equity capital (i.e., Tier 1 capital) during such period. |

| · | Assessment Rate. An institution’s assessment rate is assigned by the FDIC on a quarterly basis. To assign an assessment rate, the FDIC designates an institution as falling into one of four risk categories, or as being a large and highly complex financial institution. The FDIC determines an institution’s risk category based on the level of the institution’s capitalization and on supervisory evaluations provided to the FDIC by the institution’s primary federal regulator. Each risk category designation contains upward and downward adjustment factors based on long-term unsecured debt and brokered deposits. Assessment rates currently range from 0.025% per annum for an institution in the lowest risk category with the maximum downward adjustment, to 0.45% per annum for an institution in the highest risk category with the maximum upward adjustment. For the fourth quarter of 2013, the Bank’s assessment rate was set at $0.0133, or $0.0532 annually, per $100 of assessment base. |

| 15 | ||

| · | the Federal Truth-In-Lending Act, governing disclosures of credit terms to consumer borrowers; |

| · | the Home Mortgage Disclosure Act, requiring financial institutions to provide information to enable the public and public officials to determine whether a financial institution is fulfilling its obligation to help meet the housing needs of the community it serves; |

| · | the Equal Credit Opportunity Act, prohibiting discrimination on the basis of race, color, religion, national origin, sex, marital status or certain other prohibited factors in all aspects of credit transactions; |

| · | the Fair Credit Reporting Act, governing the use and provision of information to credit reporting agencies; |

| · | the Fair Debt Collection Act, governing the manner in which consumer debts may be collected by debt collectors; |

| · | the Servicemembers’ Civil Relief Act, governing the repayment terms of, and property rights underlying, secured obligations of persons in military service; |

| · | Rules and regulations of the various federal agencies charged with the responsibility of implementing these federal laws. |

| · | the Right to Financial Privacy Act, which imposes a duty to maintain confidentiality of consumer financial records and prescribes procedures for complying with administrative subpoenas of financial records; and |

| · | the Electronic Funds Transfer Act and Regulation E issued by the Consumer Financial Protection Bureau to implement that act, which govern automatic deposits to and withdrawals from deposit accounts and customers’ rights and liabilities arising from the use of automated teller machines and other electronic banking services. |

| 16 | ||

| 17 | ||

| · | A new common equity tier 1 capital to risk-weighted assets ratio of at least 7.0%, inclusive of a 4.5% minimum common equity tier 1 capital ratio, net of regulatory deductions, and a new 2.5% “capital conservation buffer” of common equity to risk-weighted assets; | |

| · | A tier 1 capital ratio of at least 8.5%, inclusive of the 2.5% capital conservation buffer; and | |

| · | A total capital ratio of at least 10.5%, inclusive of the 2.5% capital conservation buffer. |

| · | 4.5% based upon CET1; |

| · | 6.0% based upon tier 1 capital; and |

| · | 8.0% based upon total regulatory capital. |

| 18 | ||

| 19 | ||

| · | a bank’s loans or extensions of credit to affiliates; |

| · | a bank’s investment in affiliates; |

| · | assets a bank may purchase from affiliates, except for real and personal property exempted by the Federal Reserve; |

| · | loans or extensions of credit made by a bank to third parties collateralized by the securities or obligations of affiliates; |

| · | a bank’s guarantee, acceptance or letter of credit issued on behalf of an affiliate; |

| · | a bank’s transactions with an affiliate involving the borrowing or lending of securities to the extent they create credit exposure to the affiliate; and |

| · | a bank’s derivative transactions with an affiliate to the extent they create credit exposure to the affiliate. |

| 20 | ||

| · | requirements for financial institutions to develop policies and procedures to identify potential identity theft and, upon the request of a consumer, place a fraud alert in the consumer’s credit file stating that the consumer may be the victim of identity theft or other fraud; |

| · | requirements for entities that furnish information to consumer reporting agencies (which would include our bank) to implement procedures and policies regarding the accuracy and integrity of the furnished information and regarding the correction of previously furnished information that is later determined to be inaccurate; |

| · | requirements for mortgage lenders to disclose credit scores to consumers; and |

| · | limitations on the ability of a business that receives consumer information from an affiliate to use that information for marketing purposes. |

| 21 | ||

| 22 | ||

| · | The Dodd-Frank Act created a new Consumer Financial Protection Bureau with broad powers to supervise and enforce consumer protection laws. The Bureau now has broad rule-making authority for a wide range of consumer protection laws that apply to all banks, including the authority to prohibit “unfair, deceptive or abusive” acts and practices. The Bureau has examination and enforcement authority over all banks with more than $10 billion in assets. Institutions with less than $10 billion in assets will continue to be examined for compliance with consumer laws by their primary bank regulator. |

| · | The Dodd-Frank Act imposed new requirements regarding the origination and servicing of residential mortgage loans. The law created a variety of new consumer protections, including limitations on the manner by which loan originators may be compensated and an obligation on the part of lenders to verify a borrower’s “ability to repay” a residential mortgage loan. Final rules implementing these latter statutory requirements are effective in 2014. |

| · | The Dodd-Frank Act eliminated the federal prohibitions on paying interest on demand deposits effective one year after the date of its enactment, thus allowing businesses to have interest-bearing checking accounts. Depending on competitive responses, this significant change to existing law could have an adverse impact on our interest expense. |

| · | The Dodd-Frank Act addresses many aspects of investor protection, corporate governance and executive compensation that will affect most U.S. publicly traded companies. The Dodd-Frank Act (i) requires publicly traded companies to give stockholders a non-binding vote on executive compensation and golden parachute payments; (ii) enhances independence requirements for compensation committee members; (iii) requires companies listed on national securities exchanges to adopt incentive-based compensation claw-back policies for executive officers; (iv) authorizes the Securities and Exchange Commission (the “SEC”) to promulgate rules that would allow stockholders to nominate their own candidates using a company’s proxy materials; and (v) directs the federal banking regulators to issue rules prohibiting incentive compensation that encourages inappropriate risks. |

| · | While insured depository institutions have long been subject to the FDIC’s resolution process, the Dodd-Frank Act creates a new mechanism for the FDIC to conduct the orderly liquidation of certain “covered financial companies,” including bank holding companies and systemically significant non-bank financial companies. Upon certain findings being made, the FDIC may be appointed receiver for a covered financial company, and would conduct an orderly liquidation of the entity. The FDIC liquidation process is modeled on the existing Federal Deposit Insurance Act bank resolution process, and generally gives the FDIC more discretion than in the traditional bankruptcy context. The FDIC has issued final rules implementing the orderly liquidation authority. |

| 23 | ||

| 24 | ||

| 25 | ||

| 26 | ||

| 27 | ||

| · | maintaining loan quality; |

| · | maintaining adequate management personnel and information systems to oversee such growth; |

| · | maintaining adequate control and compliance functions; and |

| · | securing capital and liquidity needed to support anticipated growth. |

| · | the sale of 40,000 shares of our senior non-cumulative perpetual preferred stock, Series A, par value $.001 per share (or “Series A Preferred Stock”) to the United States Department of the Treasury (“Treasury”) in connection with the Treasury’s Small Business Lending Fund program for gross proceeds of $40,000,000 on June 21, 2011; |

| · | the sale of an aggregate of 340,000 shares of our common stock at $30 per share, or $10,200,000, in a private placement completed on June 30, 2011; |

| · | the sale of $20,000,000 in 5.5% subordinated notes due November 9, 2022 to accredited investor purchasers, the proceeds of which were used to pay off $15,000,000 in our 8.5% subordinated debentures; and |

| · | the sale of an aggregate of 250,000 shares of our common stock at $41.50 per share, or $10,375,000, in a private placement completed on December 2, 2013. |

| 28 | ||

| · | our ability to build and maintain long-term customer relationships while ensuring high ethical standards and safe and sound banking practices; |

| · | the scope, relevance and pricing of products and services that we offer; |

| · | customer satisfaction with our products and services; |

| · | industry and general economic trends; and |

| · | our ability to keep pace with technological advances and to invest in new technology. |

| 29 | ||

| 30 | ||

| · | general or local economic conditions; |

| · | environmental cleanup liability; |

| · | neighborhood assessments; |

| · | interest rates; |

| · | real estate tax rates; |

| · | operating expenses of the mortgaged properties; |

| · | supply of and demand for rental units or properties; |

| · | ability to obtain and maintain adequate occupancy of the properties; |

| · | zoning laws; |

| · | governmental and regulatory rules; |

| · | fiscal policies; and |

| · | natural disasters. |

| 31 | ||

| 32 | ||

| 33 | ||

| 34 | ||

| 35 | ||

| 36 | ||

| 37 | ||

| 38 | ||

| · | provide that special meetings of stockholders may be called at any time by the Chairman of our board of directors, by the President or by order of the board of directors; |

| · | enable our board of directors to issue preferred stock up to the authorized amount, with such preferences, limitations and relative rights, including voting rights, as may be determined from time to time by the board; |

| · | enable our board of directors to increase the number of persons serving as directors and to fill the vacancies created as a result of the increase by a majority vote of the directors present at the meeting; |

| · | enable our board of directors to amend our bylaws without stockholder approval; and |

| · | do not provide for cumulative voting rights (therefore allowing the holders of a majority of the shares of common stock entitled to vote in any election of directors to elect all of the directors standing for election, if they should so choose). |

|

State

|

|

|

|

|

|

|

|

|

|

|

MSA

|

|

|

|

|

|

Owned or

|

|

|

|

|

Office Address

|

|

City

|

|

Zip Code

|

|

Leased

|

|

Date Opened

|

|

|

Alabama:

|

|

|

|

|

|

|

|

|

|

|

Birmingham-Hoover:

|

|

|

|

|

|

|

|

|

|

|

850 Shades Creek Parkway, Suite 200 (1)

|

|

Birmingham

|

|

35209

|

|

Leased

|

|

3/2/2005

|

|

|

324 Richard Arrington Jr. Boulevard North

|

|

Birmingham

|

|

35203

|

|

Leased

|

|

12/19/2005

|

|

|

5403 Highway 280, Suite 401

|

|

Birmingham

|

|

35242

|

|

Leased

|

|

8/15/2006

|

|

|

Total

|

|

|

|

3 Offices

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Huntsville:

|

|

|

|

|

|

|

|

|

|

|

401 Meridian Street, Suite 100

|

|

Huntsville

|

|

35801

|

|

Leased

|

|

11/21/2006

|

|

|

1267 Enterprise Way, Suite A (1)

|

|

Huntsville

|

|

35806

|

|

Leased

|

|

8/21/2006

|

|

|

Total

|

|

|

|

2 Offices

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Montgomery:

|

|

|

|

|

|

|

|

|

|

|

1 Commerce Street, Suite 200

|

|

Montgomery

|

|

36104

|

|

Leased

|

|

6/4/2007

|

|

|

8117 Vaughn Road, Unit 20

|

|

Montgomery

|

|

36116

|

|

Leased

|

|

9/26/2007

|

|

|

Total

|

|

|

|

2 Offices

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dothan:

|

|

|

|

|

|

|

|

|

|

|

4801 West Main Street (1)

|

|

Dothan

|

|

36305

|

|

Leased

|

|

10/17/2008

|

|

|

1640 Ross Clark Circle

|

|

Dothan

|

|

36301

|

|

Leased

|

|

2/1/2011

|

|

|

Total

|

|

|

|

2 Offices

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mobile:

|

|

|

|

|

|

|

|

|

|

|

64 North Royal Street

|

|

Mobile

|

|

36602

|

|

Leased

|

|

7/9/2012

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Offices in Alabama

|

|

|

|

9 Offices

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Florida:

|

|

|

|

|

|

|

|

|

|

|

Pensacola-Ferry Pass-Brent:

|

|

|

|

|

|

|

|

|

|

|

316 South Balen Street

|

|

Pensacola

|

|

32502

|

|

Leased

|

|

4/1/2011

|

|

|

4980 North 12th Avenue

|

|

Pensacola

|

|

32504

|

|

Owned

|

|

8/27/2012

|

|

|

Total

|

|

|

|

2 Offices

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tennessee:

|

|

|

|

|

|

|

|

|

|

|

Nashville:

|

|

|

|

|

|

|

|

|

|

|

611 Commerce Street (2)

|

|

Nashville

|

|

37203

|

|

Leased

|

|

6/4/2013

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total offices

|

|

|

|

13 Offices

|

|

|

|

|

|

| 39 | ||

| 40 | ||

|

Plan Category

|

|

Number of Securities

Issued/To Be Issued Upon Exercise of Outstanding Awards |

|

|

Weighted-average

Exercise Price of Outstanding Awards |

|

Number of Securities

Remaining Available For Future Issuance Under Equity Compensation Plans |

|

|

Equity Compensation Award-Plans Approved by Security Holders

|

|

806,500

|

|

$

|

24.15

|

|

217,670

|

|

|

Equity Compensation Awards-Plans Not Approved by Security Holders

|

|

48,300

|

|

|

17.59

|

|

-

|

|

|

Total

|

|

854,800

|

|

$

|

23.77

|

|

217,670

|

|

| 41 | ||

|

|

|

Date

|

|

||||||||||

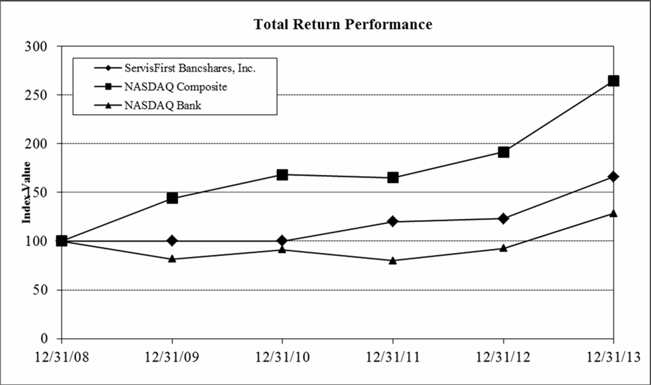

|

Index:

|

|

12/31/2008

|

|

12/31/2009

|

|

12/31/2010

|

|

12/31/2011

|

|

12/31/2012

|

|

12/31/2013

|

|

|

ServisFirst Bancshares, Inc.

|

|

100.00

|

|

100.00

|

|

100.00

|

|

120.00

|

|

123.00

|

|

166.00

|

|

|

NASDAQ Composite

|

|

100.00

|

|

143.89

|

|

168.22

|

|

165.19

|

|

191.47

|

|

264.84

|

|

|

NASDAQ Bank

|

|

100.00

|

|

81.50

|

|

91.18

|

|

79.85

|

|

92.46

|

|

128.43

|

|

| 42 | ||

|

|

|

As of and for the years ended December 31,

|

|

|||||||||||||||||

|

|

|

2013

|

|

|

2012

|

|

|

2011

|

|

|

2010

|

|

|

2009

|

|

|||||

|

|

|

(Dollars in thousands except for share and per share data)

|

|

|||||||||||||||||

|

Selected Balance Sheet Data:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Assets

|

|

$

|

3,520,699

|

|

|

$

|

2,906,314

|

|

|

$

|

2,460,785

|

|

|

$

|

1,935,166

|

|

|

$

|

1,573,497

|

|

|

Total Loans

|

|

|

2,858,868

|

|

|

|

2,363,182

|

|

|

|

1,830,742

|

|

|

|

1,394,818

|

|

|

|

1,207,084

|

|

|

Loans, net

|

|

|

2,828,205

|

|

|

|

2,336,924

|

|

|

|

1,808,712

|

|

|

|

1,376,741

|

|

|

|

1,192,173

|

|

|

Securities available for sale

|

|

|

266,220

|

|

|

|

233,877

|

|

|

|

293,809

|

|

|

|

276,959

|

|

|

|

255,453

|

|

|

Securities held to maturity

|

|

|

32,274

|

|

|

|

25,967

|

|

|

|

15,209

|

|

|

|

5,234

|

|

|

|

645

|

|

|

Cash and due from banks

|

|

|

61,370

|

|

|

|

58,031

|

|

|

|

43,018

|

|

|

|

27,454

|

|

|

|

26,982

|

|

|

Interest-bearing balances with banks

|

|

|

188,411

|

|

|

|

119,423

|

|

|

|

99,350

|

|

|

|

204,278

|

|

|

|

48,544

|

|

|

Fed funds sold

|

|

|

8,634

|

|

|

|

3,291

|

|

|

|

100,565

|

|

|

|

346

|

|

|

|

680

|

|

|

Mortgage loans held for sale

|

|

|

8,134

|

|

|

|

25,826

|

|

|

|

17,859

|

|

|

|

7,875

|

|

|

|

6,202

|

|

|

Restricted equity securities

|

|

|

3,738

|

|

|

|

3,941

|

|

|

|

3,501

|

|

|

|

3,510

|

|

|

|

3,241

|

|

|

Premises and equipment, net

|

|

|

8,351

|

|

|

|

8,847

|

|

|

|

4,591

|

|

|

|

4,450

|

|

|

|

5,088

|

|

|

Deposits

|

|

|

3,019,642

|

|

|

|

2,511,572

|

|

|

|

2,143,887

|

|

|

|

1,758,716

|

|

|

|

1,432,355

|

|

|

Other borrowings

|

|

|

194,320

|

|

|

|

136,982

|

|

|

|

84,219

|

|

|

|

24,937

|

|

|

|

24,922

|

|

|

Subordinated debentures

|

|

|

-

|

|

|

|

15,050

|

|

|

|

30,514

|

|

|

|

30,420

|

|

|

|

15,228

|

|

|

Other liabilities

|

|

|

9,545

|

|

|

|

9,453

|

|

|

|

5,873

|

|

|

|

3,993

|

|

|

|

3,370

|

|

|

Stockholders' Equity

|

|

|

297,192

|

|

|

|

233,257

|

|

|

|

196,292

|

|

|

|

117,100

|

|

|

|

97,622

|

|

|

Selected income Statement Data:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest income

|

|

$

|

126,081

|

|

|

$

|

109,023

|

|

|

$

|

91,411

|

|

|

$

|

78,146

|

|

|

$

|

62,197

|

|

|

Interest expense

|

|

|

13,619

|

|

|

|

14,901

|

|

|

|

16,080

|

|

|

|

15,260

|

|

|

|

18,337

|

|

|

Net interest income

|

|

|

112,462

|

|

|

|

94,122

|

|

|

|

75,331

|

|

|

|

62,886

|

|

|

|

43,860

|

|

|

Provision for loan losses

|

|

|

13,008

|

|

|

|

9,100

|

|

|

|

8,972

|

|

|

|

10,350

|

|

|

|

10,685

|

|

|

Net interest income after provision for loan losses

|

|

|

99,454

|

|

|

|

85,022

|

|

|

|

66,359

|

|

|

|

52,536

|

|

|

|

33,175

|

|

|

Noninterest income

|

|

|

10,010

|

|

|

|

9,643

|

|

|

|

6,926

|

|

|

|

5,169

|

|

|

|

4,413

|

|

|

Noninterest expense

|

|

|

47,489

|

|

|

|

43,100

|

|

|

|

37,458

|

|

|

|

30,969

|

|

|

|

28,930

|

|

|

Income before income taxes

|

|

|

61,975

|

|

|

|

51,565

|

|

|

|

35,827

|

|

|

|

26,736

|

|

|

|

8,658

|

|

|

Income taxes expenses

|

|

|

20,358

|

|

|

|

17,120

|

|

|

|

12,389

|

|

|

|

9,358

|

|

|

|

2,780

|

|

|

Net income

|

|

|

41,617

|

|

|

|

34,445

|

|

|

|

23,438

|

|

|

|

17,378

|

|

|

|

5,878

|

|

|

Net income available to common stockholders

|

|

|

41,201

|

|

|

|

34,045

|

|

|

|

23,238

|

|

|

|

17,378

|

|

|

|

5,878

|

|

|

Per common Share Data:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income, basic

|

|

$

|

6.00

|

|

|

$

|

5.68

|

|

|

$

|

4.03

|

|

|

$

|

3.15

|

|

|

$

|

1.07

|

|

|

Net income, diluted

|

|

|

5.69

|

|

|

|

4.99

|

|

|

$

|

3.53

|

|

|

$

|

2.84

|

|

|

$

|

1.02

|

|

|

Book value

|

|

|

35.00

|

|

|

|

30.84

|

|

|

$

|

26.34

|

|

|

$

|

21.19

|

|

|

$

|

17.71

|

|

|

Weighted average shares outstanding:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic

|

|

|

6,869,071

|

|

|

|

5,996,437

|

|

|

|

5,759,524

|

|

|

|

5,519,151

|

|

|

|

5,485,972

|

|

|

Diluted

|

|

|

7,268,675

|

|

|

|

6,941,752

|

|

|

|

6,749,163

|

|

|

|

6,294,604

|

|

|

|

5,787,643

|

|

|

Actual shares outstanding

|

|

|

7,346,512

|

|

|

|

6,268,812

|

|

|

|

5,932,182

|

|

|

|

5,527,482

|

|

|

|

5,513,482

|

|

|

Selected Performance Ratios:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return on average assets

|

|

|

1.31

|

%

|

|

|

1.30

|

%

|

|

|

1.11

|

%

|

|

|

1.04

|

%

|

|

|

0.43

|

%

|

|

Return on average stockholders' equity

|

|

|

15.55

|

%

|

|

|

15.81

|

%

|

|

|

14.73

|

%

|

|

|

15.86

|

%

|

|

|

6.33

|

%

|

|

Dividend payout ratio

|

|

|

8.79

|

%

|

|

|

10.02

|

%

|

|

|

-

|

%

|

|

|

-

|

%

|

|

|

-

|

%

|

|

Net interest margin (1)

|

|

|

3.80

|

%

|

|

|

3.80

|

%

|

|

|

3.79

|

%

|

|

|

3.94

|

%

|

|

|

3.31

|

%

|

|

Efficiency ratio (2)

|

|

|

38.78

|

%

|

|

|

41.54

|

%

|

|

|

45.54

|

%

|

|

|

45.51

|

%

|

|

|

59.57

|

%

|

|

Asset quality Ratios:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net charge-offs to average loans outstanding

|

|

|

0.33

|

%

|

|

|

0.24

|

%

|

|

|

0.32

|

%

|

|

|

0.55

|

%

|

|

|

0.60

|

%

|

|

Non-performing loans to totals loans

|

|

|

0.34

|

%

|

|

|

0.44

|

%

|

|

|

0.75

|

%

|

|

|

1.03

|

%

|

|

|

1.01

|

%

|

|

Non-performing assets to total assets

|

|

|

0.64

|

%

|

|

|

0.69

|

%

|

|

|

1.06

|

%

|

|

|

1.10

|

%

|

|

|

1.57

|

%

|

|

Allowance for loan losses to total gross loans

|

|

|

1.07

|

%

|

|

|

1.11

|

%

|

|

|

1.20

|

%

|

|

|

1.30

|

%

|

|

|

1.24

|

%

|

|

Allowance for loan losses to total non-performing loans

|

|

|

314.94

|

%

|

|

|

253.50

|

%

|

|

|

159.96

|

%

|

|

|

126.00

|

%

|

|

|

122.34

|

%

|

|

Liquidity Ratios:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net loans to total deposits

|

|

|

93.66

|

%

|

|

|

93.05

|

%

|

|

|

84.37

|

%

|

|

|

78.28

|

%

|

|

|

83.23

|

%

|

|

Net average loans to average earning assets

|

|

|

84.65

|

%

|

|

|

79.82

|

%

|

|

|

76.71

|

%

|

|

|

78.04

|

%

|

|

|

80.06

|

%

|

|

Noninterest-bearing deposits to total deposits

|

|

|

21.54

|

%

|

|

|

21.71

|

%

|

|

|

16.96

|

%

|

|

|

14.24

|

%

|

|

|

14.75

|

%

|

|

Capital Adequacy Ratios:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stockholders' Equity to total assets

|

|

|

8.44

|

%

|

|

|

8.03

|

%

|

|

|

7.97

|

%

|

|

|

6.05

|

%

|

|

|

6.20

|

%

|

|

Total risked-based capital (3)

|

|

|

11.73

|

%

|

|

|

11.78

|

%

|

|

|

12.79

|

%

|

|

|

11.82

|

%

|

|

|

10.48

|

%

|

|

Tier 1 capital (4)

|

|

|

10.00

|

%

|

|

|

9.89

|

%

|

|

|

11.39

|

%

|

|

|

10.22

|

%

|

|

|

8.89

|

%

|

|

Leverage ratio (5)

|

|

|

8.48

|

%

|

|

|

8.43

|

%

|

|

|

9.17

|

%

|

|

|

7.77

|

%

|

|

|

6.97

|

%

|

|

Growth Ratios:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Percentage change in net income

|

|

|

20.82

|

%

|

|

|

46.96

|

%

|

|

|

34.87

|

%

|

|

|

195.64

|

%

|

|

|

(16.10)

|

%

|

|

Percentage change in diluted net income per share

|

|

|

14.03

|

%

|

|

|

41.36

|

%

|

|

|

24.30

|

%

|

|

|

178.43

|

%

|

|

|

(22.14)

|

%

|

|

Percentage change in assets

|

|

|

21.14

|

%

|

|

|

18.11

|

%

|

|

|

27.16

|

%

|

|

|

22.99

|

%

|

|

|

35.38

|

%

|

|

Percentage change in net loans

|

|

|

21.02

|

%

|

|

|

29.20

|

%

|

|

|

31.38

|

%

|

|

|

15.48

|

%

|

|

|

24.49

|

%

|

|

Percentage change in deposits

|

|

|

20.23

|

%

|

|

|

17.15

|

%

|

|

|

21.90

|

%

|

|

|

22.78

|

%

|

|

|

38.08

|

%

|

|

Percentage change in equity

|

|

|

27.41

|

%

|

|

|

18.83

|

%

|

|

|

67.63

|

%

|

|

|

19.95

|

%

|

|

|

12.49

|

%

|

| 43 | ||

| 44 | ||

| 45 | ||

|

|

|

For the years ended December 31,

|

|

||||

|

|

|

2013

|

|

2012

|

|

2011

|

|

|

Return on average assets

|

|

1.31

|

%

|

1.30

|

%

|

1.11

|

%

|

|

Return on average stockholders' equity

|

|

15.55

|

%

|

15.81

|

%

|

14.73

|

%

|

|

Dividend payout ratio

|

|

8.79

|

%

|

10.02

|

%

|

-

|

%

|

|

Average stockholders' equity to

average total assets |

|

8.43

|

%

|

8.19

|

%

|

7.56

|

%

|

|

|

|

|

Year Ended December 31,

|

|

|

|

|

|||||

|

|

|

|

2013

|

|

|

2012

|

|

Change from

the Prior Year |

|

|||

|

|

|

|

(Dollars in Thousands)

|

|

|

|

|

|||||

|

Interest income

|

|

|

$

|

126,081

|

|

|

$

|

109,023

|

|

|

15.65

|

%

|

|

Interest expense

|

|

|

|

13,619

|

|

|

|

14,901

|

|

|

-8.60

|

%

|

|

Net interest income

|

|

|

|

112,462

|

|

|

|

94,122

|

|

|

19.49

|

%

|

|

Provision for loan losses

|

|

|

|

13,008

|

|

|

|

9,100

|

|

|

42.95

|

%

|

|

Net interest income after

provision for loan losses |

|

|

|

99,454

|

|

|

|

85,022

|

|

|

16.97

|

%

|

|

Noninterest income

|

|

|

|

10,010

|

|

|

|

9,643

|

|

|

3.81

|

%

|

|

Noninterest expense

|

|

|

|

47,489

|

|

|

|

43,100

|

|

|

10.18

|

%

|

|

Net income before taxes

|

|

|

|

61,975

|

|

|

|

51,565

|

|

|

20.19

|

%

|

|

Taxes

|

|

|

|

20,358

|

|

|

|

17,120

|

|

|

18.91

|

%

|

|

Net income

|

|

|

|

41,617

|

|

|

|

34,445

|

|

|

20.82

|

%

|

|

Dividends on preferred stock

|

|

|

|

416

|

|

|

|

400

|

|

|

4.00

|

%

|

|

Net income available to

common stockholders |

|

|

$

|

41,201

|

|

|

$

|

34,045

|

|

|

21.02

|

%

|

|

|

|

Year Ended December 31,

|

|

|

|

|

||||

|

|

|

2012

|

|

2011

|

|

Change from

the Prior Year |

|

|||

|

|

|

(Dollars in Thousands)

|

|

|

|

|

||||

|

Interest income

|

|

$

|

109,023

|

|

$

|

91,411

|

|

|

19.27

|

%

|

|

Interest expense

|

|

|

14,901

|

|

|

16,080

|

|

|

-7.33

|

%

|

|

Net interest income

|

|

|

94,122

|

|

|

75,331

|

|

|

24.94

|

%

|

|

Provision for loan losses

|

|

|

9,100

|

|

|

8,972

|

|

|

1.43

|

%

|

|

Net interest income after

provision for loan losses |

|

|

85,022

|

|

|

66,359

|

|

|

28.12

|

%

|

|

Noninterest income

|

|

|

9,643

|

|

|

6,926

|

|

|

39.23

|

%

|

|

Noninterest expense

|

|

|

43,100

|

|

|

37,458

|

|

|

15.06

|

%

|

|

Net income before taxes

|

|

|

51,565

|

|

|

35,827

|

|

|

43.93

|

%

|

|

Taxes

|

|

|

17,120

|

|

|

12,389

|

|

|

38.19

|

%

|

|

Net income

|

|

|

34,445

|

|

|

23,438

|

|

|

46.96

|

%

|

|

Dividends on preferred stock

|

|

|

400

|

|

|

200

|

|

|

100.00

|

%

|

|

Net income available to

common stockholders |

|

$

|

34,045

|

|

$

|

23,238

|

|

|

46.51

|

%

|

| 46 | ||

| 47 | ||

|

|

|

2013

|

|

2012

|

|

2011

|

|

||||||||||||||||||

|

|

|

Average

Balance |

|

Interest

Earned / Paid |

|

Average

Yield / Rate |

|

Average

Balance |

|

Interest

Earned / Paid |

|

Average

Yield / Rate |

|

Average

Balance |

|

Interest

Earned / Paid |

|

Average

Yield / Rate |

|

||||||

|

Assets:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-earning assets:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans, net of unearned income

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxable (1)

|

|

$

|

2,573,621

|

|

$

|

118,032

|

|

4.59

|

%

|

$

|

2,034,478

|

|

$

|

100,143

|

|

4.92

|

%

|

$

|

1,573,500

|

|

$

|

82,083

|

|

5.22

|

%

|

|

Tax-exempt (2)

|

|

|

3,274

|

|

|

170

|

|

5.19

|

|

|

1,631

|

|

|

95

|

|

5.82

|

|

|

-

|

|

|

-

|

|

-

|

|

|

Mortgage loans held for sale

|

|

|

12,953

|

|

|

306

|

|

2.36

|

|

|

17,905

|

|

|

349

|

|

1.95

|

|

|

7,556

|

|

|

211

|

|

2.79

|

|

|

Securities:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxable

|

|

|

149,996

|

|

|

3,906

|

|

2.60

|

|

|

184,174

|

|

|

4,815

|

|

2.61

|

|

|

188,315

|

|

|

5,721

|

|

3.04

|

|

|

Tax-exempt (2)

|

|

|

115,829

|

|

|

4,884

|

|

4.22

|

|

|

100,926

|

|

|

4,683

|

|

4.64

|

|

|

82,239

|

|

|

4,275

|

|

5.20

|

|

|

Total securities (3)

|

|

|

265,825

|

|

|

8,790

|

|

3.31

|

|

|

285,100

|

|

|

9,498

|

|

3.33

|

|

|

270,554

|

|

|

9,996

|

|

3.69

|

|

|

Federal funds sold

|

|

|

44,106

|

|

|

110

|

|

0.25

|

|

|

94,425

|

|

|

196

|

|

0.21

|

|

|

85,825

|

|

|

176

|

|

0.21

|

|

|

Restricted equity securities

|

|

|

4,299

|

|

|

93

|

|

2.16

|

|

|

4,434

|

|

|

104

|

|

2.35

|

|

|

4,259

|

|

|

74

|

|

1.74

|

|

|

Interest-bearing balances with banks

|

|

|

100,417

|

|

|

280

|

|

0.28

|

|

|

80,170

|

|

|

200

|

|

0.25

|

|

|

83,152

|

|

|

203

|

|

0.24

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total interest-earning assets

|

|

$

|

3,004,495

|

|

$

|

127,781

|

|

4.25

|

%

|

$

|

2,518,143

|

|

$

|

110,585

|

|

4.39

|

%

|

$

|

2,024,846

|

|

$

|

92,743

|

|

4.58

|

%

|

|

Non-interest-earning assets:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and due from banks

|

|

|

45,528

|

|

|

|

|

|

|

|

38,467

|

|

|

|

|

|

|

|

28,304

|

|

|

|

|

|

|

|

Net premises and equipment

|

|

|

9,148

|

|

|

|

|

|

|

|

6,074

|

|

|

|

|

|

|

|

4,813

|

|

|

|

|

|

|

|

Allowance for loan losses,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

accrued interest and

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

other assets

|

|

|

84,297

|

|

|

|

|

|

|

|

65,504

|

|

|

|

|

|

|

|

29,094

|

|

|

|

|

|

|

|

Total assets

|

|

$

|

3,143,468

|

|

|

|

|

|

|

$

|

2,628,188

|

|

|

|

|

|

|

$

|

2,087,057

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing liabilities:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing deposits:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Checking

|

|

$

|

433,931

|

|

$

|

1,201

|

|

0.28

|

%

|

$

|

351,975

|

|

$

|

1,074

|

|

0.31

|

%

|

$

|

303,165

|

|

$

|

1,133

|

|

0.37

|

%

|

|

Savings

|

|

|

21,793

|

|

|

61

|

|

0.28

|

|

|

17,081

|

|

|

48

|

|

0.28

|

|

|

10,088

|

|

|

47

|

|

0.47

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Money market

|

|

|

1,244,957

|

|

|

5,810

|

|

0.47

|

|

|

1,042,870

|

|

|

5,820

|

|

0.56

|

|

|

902,290

|

|

|

6,675

|

|

0.74

|

|

|

Time deposits

|

|

|

404,927

|

|

|

4,758

|

|

1.18

|

|

|

398,552

|

|

|

5,307

|

|

1.33

|

|

|

330,221

|

|

|

5,192

|

|

1.57

|

|

|

Federal funds purchased

|

|

|

167,063

|

|

|

462

|

|

0.28

|

|

|

88,732

|

|

|

222

|

|

0.25

|

|

|

19,335

|

|

|

49

|

|

0.25

|

|

|

Other borrowings

|

|

|

21,780

|

|

|

1,327

|

|

6.09

|

|

|

33,126

|

|

|

2,430

|

|

7.34

|

|

|

41,866

|

|

|

2,984

|

|

7.13

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total interest-bearing liabilities

|

|

$

|

2,294,451

|

|

$

|

13,619

|

|

0.59

|

%

|

$

|

1,932,336

|

|

$

|

14,901

|

|

0.77

|

%

|

$

|

1,606,965

|

|

$

|

16,080

|

|

1.00

|

%

|

|

Non-interest-bearing liabilities:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non-interest-bearing

checking |

|

|

576,072

|

|

|

|

|

|

|

|

474,284

|

|

|

|

|

|

|

|

315,781

|

|

|

|

|

|

|

|

Other liabilities

|

|

|

7,835

|

|

|

|

|

|

|

|

6,200

|

|

|

|

|

|

|

|

6,580

|

|

|

|

|

|

|

|

Stockholders' equity

|

|

|

259,631

|

|

|

|

|

|

|

|

207,656

|

|

|

|

|

|

|

|

145,050

|

|

|

|

|

|

|

|

Unrealized gains on securities

and derivatives |

|

|

5,479

|

|

|

|

|

|

|

|

7,712

|

|

|

|

|

|

|

|

12,681

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total liabilities and

stockholders' equity |

|

$

|

3,143,468

|

|

|

|

|

|

|

$

|

2,628,188

|

|

|

|

|

|

|

$

|

2,087,057

|

|

|

|

|

|

|

|

Net interest spread

|

|

|

|

|

|

|

|

3.66

|

%

|

|

|

|

|

|

|

3.62

|

%

|

|

|

|

|

|

|

3.58

|

%

|

|

Net interest margin

|

|

|

|

|

|

|

|

3.80

|

%

|

|

|

|

|

|

|

3.80

|

%

|

|

|

|

|

|

|

3.79

|

%

|

|

(1)

|

Non-accrual loans are included in average loan balances in all periods. Loan fees of $551,000, $372,000 and $538,000 are included in interest income in 2013, 2012 and 2011, respectively.

|

|

(2)

|

Interest income and yields are presented on a fully taxable equivalent basis using a tax rate of 35%.

|

|

(3)

|

Unrealized gains of $8,408,000, $11,998,000 and $7,624,000 are excluded from the yield calculation in 2013, 2012 and 2011, respectively.

|

| 48 | ||

|

|

|

For the Year Ended December 31,

|

|

||||||||||||||||

|

|

|

2013 Compared to 2012 Increase (Decrease) in Interest

Income and Expense Due to Changes in: |

|

2012 Compared to 2011 Increase (Decrease) in Interest

Income and Expense Due to Changes in: |

|

||||||||||||||

|

|

|

Volume

|

|

Rate

|

|

Total

|

|

Volume

|

|

Rate

|

|

Total

|

|

||||||

|

Interest-earning assets:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans, net of unearned income

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxable

|

|

$

|

25,097

|

|

$

|

(7,208)

|

|

$

|

17,889

|

|

$

|

22,910

|

|

$

|

(4,850)

|

|

$

|

18,060

|

|

|

Tax-exempt

|

|

|

86

|

|

|

(11)

|

|

|

75

|

|

|

95

|

|

|

-

|

|

|

95

|

|

|

Mortgages held for sale

|

|

|

(108)

|

|

|

65

|

|

|

(43)

|

|

|

218

|

|

|

(80)

|

|

|

138

|

|

|

Taxable

|

|

|

(890)

|

|

|

(19)

|

|

|

(909)

|

|

|

(124)

|

|

|

(782)

|

|

|

(906)

|

|

|

Tax-exempt

|

|

|

652

|

|

|

(451)

|

|

|

201

|

|

|

900

|

|

|

(492)

|

|

|

408

|

|

|

Federal funds sold

|

|

|

(119)

|

|

|

33

|

|

|

(86)

|

|

|

18

|

|

|

2

|

|

|

20

|

|

|

Restricted equity securities

|

|

|

(3)

|

|

|

(8)

|

|

|

(11)

|